Tax Tip #285

Ralph Loggia • February 10, 2026

W-9 Guidelines for Disregarded Entities

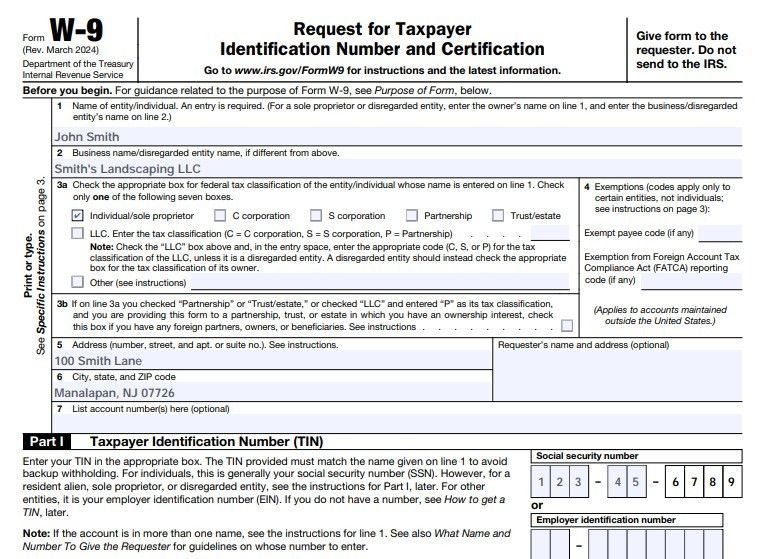

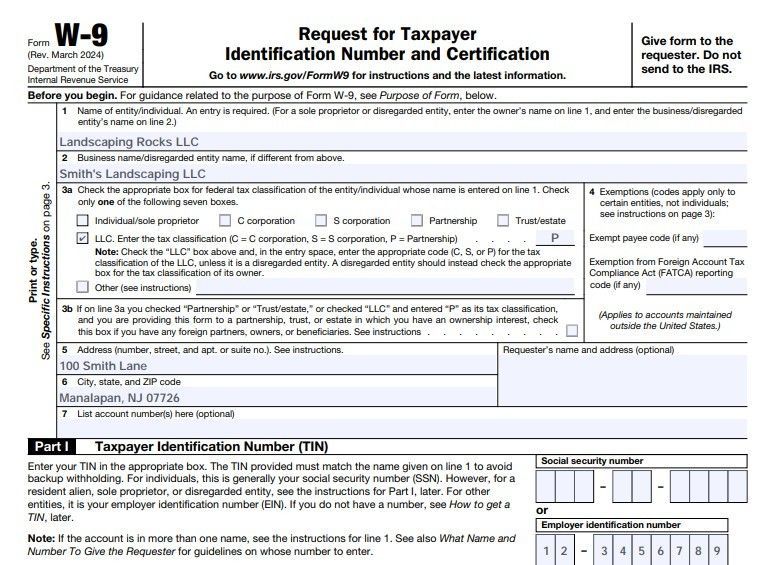

W-9s can be a bit tricky when preparing one for a disregarded entity (DE). It is important to include the information of the individual/entity that is filing the tax return in which the activity of the DE is being reported. For instance, if a DE is owned by an individual, include both the DE’s information as well as the individual owner.

- Line 1 – Name of the individual/entity owning the DE. If the direct owner of the DE is also a DE, enter the first owner that is not a DE for federal tax purposes. (ex: One, LLC is a DE owned by Two, LLC and Two, LLC is a DE owned by Three, LLC. Since Three, LLC is the first entity that is not a DE, enter that on Line 1.)

- Line 2 – The disregarded entity

- Line 3a – Check the box that describes type of ownership - Individual, C-Corp, S-Corp, Partnership, Trust/Estate or LLC. (Note: If an LLC owns the DE, the LLC box should be checked and the tax classification of either C-Corp, S-Corp, or Partnership would have to be indicated as well.)

- Line 5 – Address of the disregarded entity.

- Part I – SSN of individual or EIN of entity listed on Line 1, not the EIN of the DE.

Example 1: John Smith owns 100% of Smith’s Landscaping LLC

Example 2: Landscaping Rocks LLC—an LLC that classifies as a partnership—owns 100% of Smith’s Landscaping LLC.

You might also like

Tax Tips

IRS Refunds No Longer Issued by Paper Check

Contribute $2,000 to an IRA - IRS Might Give You $1,000

NY Minimum Wages Increases in ‘26